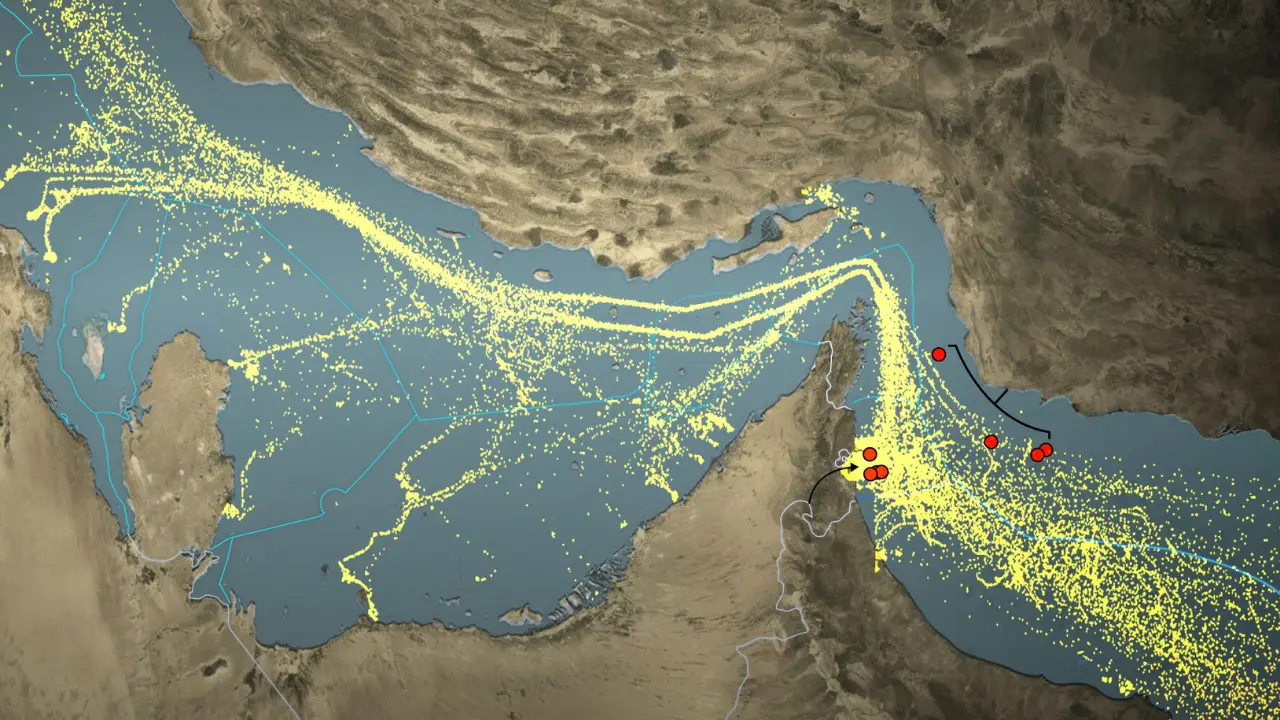

The Strait of Hormuz constitutes the most critical maritime chokepoint for global energy and trade flows. As the sole maritime outlet of the Persian Gulf, it facilitates the transit of approximately one-fifth of the world’s petroleum liquids and liquefied natural gas, rendering it indispensable for global economic stability. By early March 2026, an escalation in Middle Eastern tensions, precipitated by military strikes and retaliatory measures, transformed the theoretical risk of closure into an immediate operational challenge. Iranian naval warnings and the withdrawal of commercial maritime insurance have created conditions equivalent to a full blockade, exposing the structural vulnerabilities of global energy supply chains and generating acute macroeconomic consequences for emerging economies, particularly in South Asia.

Geographically, the Strait measures roughly 33 kilometers at its narrowest point, yet functional navigation occurs within two-mile-wide channels for inbound and outbound traffic, separated by a two-mile buffer. This spatial concentration magnifies susceptibility to physical interdiction, asymmetric harassment, and strategic deployment of naval mines. In 2024 and through early 2025, daily flows averaged 20 million barrels, representing roughly 20 percent of global petroleum liquids consumption and over one-quarter of seaborne oil trade. Saudi Arabia contributed approximately 7.1 million barrels per day, followed by Iraq at 3.6 million barrels, the United Arab Emirates at 3.4 million barrels, Kuwait at 2.4 million barrels, Iran at 1.8 million barrels, Qatar at 1.5 million barrels, Bahrain at 0.2 million barrels, and the Neutral Zone at 0.3 million barrels. The flow comprised crude oil, condensates, and refined products, forming the backbone of industrial and power-generation hubs across Asia.

The Strait also serves as the primary conduit for Qatari and Emirati liquefied natural gas, representing roughly 20 percent of global LNG trade. Limited pipeline alternatives for the majority of Gulf LNG exports produce a structural dependency that magnifies the strategic importance of uninterrupted maritime access, leaving gas-importing nations highly exposed to disruptions.

Mechanisms of Disruption and Market Impact

The 2026 crisis evolved after targeted U.S. and Israeli strikes against Iranian government and military facilities, referred to as Operation Epic Fury. Iran responded by leveraging the Strait as a strategic instrument, issuing warnings that prohibited vessel transits, effectively weaponizing commerce. The global insurance market reacted by withdrawing coverage or imposing extreme war-risk premiums, raising voyage costs by up to $500,000 per vessel. Major shipping lines, including Maersk, MSC, and Hapag-Lloyd, suspended transits, leaving approximately 150-170 vessels immobilized and halting roughly one-fifth of global seaborne energy flows.

Upstream production faces immediate constraints. Gulf producers, including Saudi Arabia, Kuwait, and Iraq, have limited storage capacity and can sustain regular output for approximately 25 days before reaching critical saturation. Initial accumulation over the first ten days allows production to continue while storage increases at export terminals. Between days 11 and 20, storage approaches maximum capacity, triggering selective output reductions. By days 21 to 25, safe operational limits are reached, necessitating mandatory production suspension. Beyond this threshold, physical storage constraints enforce total production stoppage, creating a dual supply shock that removes both the 20 million barrels per day of active flow and an additional 3 to 5 million barrels of global spare capacity, much of it trapped behind the Strait.

Energy markets reacted immediately, incorporating a geopolitical risk premium into prices. Brent crude, trading in the high $60s to low $70s before the escalation, surged over 10 percent within hours. Short-term projections anticipate stabilization between $80 and $95 per barrel, while prolonged disruption could elevate prices above $100, with extreme scenarios ranging to $200-$300 per barrel, echoing the systemic shock of the 1973 oil embargo.

Natural gas markets face structural pressure due to the lack of alternative export routes for Qatari LNG. A protracted closure could reduce global LNG supply by 15-20 percent, potentially tripling European wholesale gas prices and triggering industrial shutdowns. Asian importers, including Japan and South Korea, may confront price surges of up to 170 percent, directly threatening industrial energy security and domestic power generation.

Regional Vulnerability and Strategic Implications

South Asian economies remain highly exposed due to elevated import dependency and constrained fiscal buffers. India, the world’s third-largest oil consumer, imports approximately 85-90 percent of its crude requirements, with 40-50 percent transiting the Strait. LNG imports account for 54-60 percent of domestic demand, supporting fertilizer production and power generation, while LPG imports exceed 85 percent of household consumption. The economic impact is immediate: for every $10 increase in crude prices, consumer price inflation rises by 0.3-0.7 percentage points, and the current account deficit expands by 0.3-0.5 percent of GDP. A sustained 25 percent rise in oil prices could inflate India’s import bill by $15 billion and reduce real GDP growth by 0.2 percent. Critical sectors, including aviation, manufacturing, fast-moving consumer goods, fertilizer supply chains, and electronics exports, face cascading vulnerabilities, with food security threatened by potential shortages in nitrogenous fertilizers essential for the kharif crop cycle.

Pakistan’s exposure, though mitigated by partial domestic energy diversification through coal and renewables, remains acute for imported oil and refined products. Strategic fuel stocks covering 28-30 days provide temporary relief, yet the surge in energy prices pressures monetary authorities to maintain tight interest rates to defend the Pakistani Rupee and preserve price stability.

Global trade disruption extends beyond energy commodities. Container carriers have rerouted through the Cape of Good Hope, adding 15-20 days to transit times and $1 million in fuel costs per voyage, reducing overall vessel availability and driving freight rates upward. Air cargo demand for high-value goods, such as pharmaceuticals and microchips, surged, inflating rates by up to 400 percent in 48 hours. Fertilizer supply disruptions threaten both regional agriculture and global food security, amplifying subsidy burdens and domestic price inflation.

Legal ambiguities complicate resolution. UNCLOS codifies transit passage rights through international straits, yet Iran, which has not ratified the convention, asserts more restrictive claims under innocent passage principles. The United States, invoking customary international law, upholds freedom of navigation, framing Iranian prohibitions as potential justification for collective self-defense.

Alternative routes provide only partial relief. Bypass pipelines in Saudi Arabia and the UAE offer a combined capacity of 2.6-3.5 million barrels per day, roughly 13-17 percent of typical Strait flows. Strategic petroleum reserves provide short-term consumption buffers but cannot shield markets from the immediate price shock.

The 2026 crisis establishes a new baseline for global energy pricing, with $100 per barrel emerging as the floor, and extended closures likely sustaining $130-150 per barrel. Asian economies confront direct threats to industrial output and financial stability. The combination of insurance withdrawal, legal uncertainty, and physical chokepoint vulnerability intensifies macroeconomic instability. Repeated disruptions reinforce the imperative for accelerated energy diversification, positioning renewable energy and nuclear power as critical components of national security.

The duration of the disruption remains the decisive variable. Fortnight-long volatility remains absorbable; month-long closure triggers systemic realignment of energy flows, maritime logistics, and macroeconomic equilibrium. For South Asia, the Strait of Hormuz is more than a geographic feature; it underpins industrial growth, fiscal stability, and energy security. The 2026 closure illustrates the profound interconnection between geopolitical tension and macroeconomic outcomes in an increasingly energy-dependent global system.